Vote YES on Amendment 5

Modernizing Missouri’s Tax System. Growing Jobs and Making Missouri Competitive Again.

Amendment 5 is our opportunity to eliminate the income tax, reduce property taxes, and unleash real economic prosperity in Missouri to compete with the other surrounding states that are also working to eliminate their state income taxes.

Missouri Must Modernize Its Outdated Tax Structure - How Amendment 5 Delivers Relief for Missourians

Missouri’s tax system is a relic of the 1930s, heavily reliant on taxing what Missourians earn and own. For 100 years, the data is clear: states without a broad income tax grow faster and attract people and businesses, while high-income-tax states stagnate or shrink. HJR 174 offers a constitutional path to break this cycle by phasing out the income tax and shifting to a modern consumption-based system that taxes what people buy — not what they earn or own.

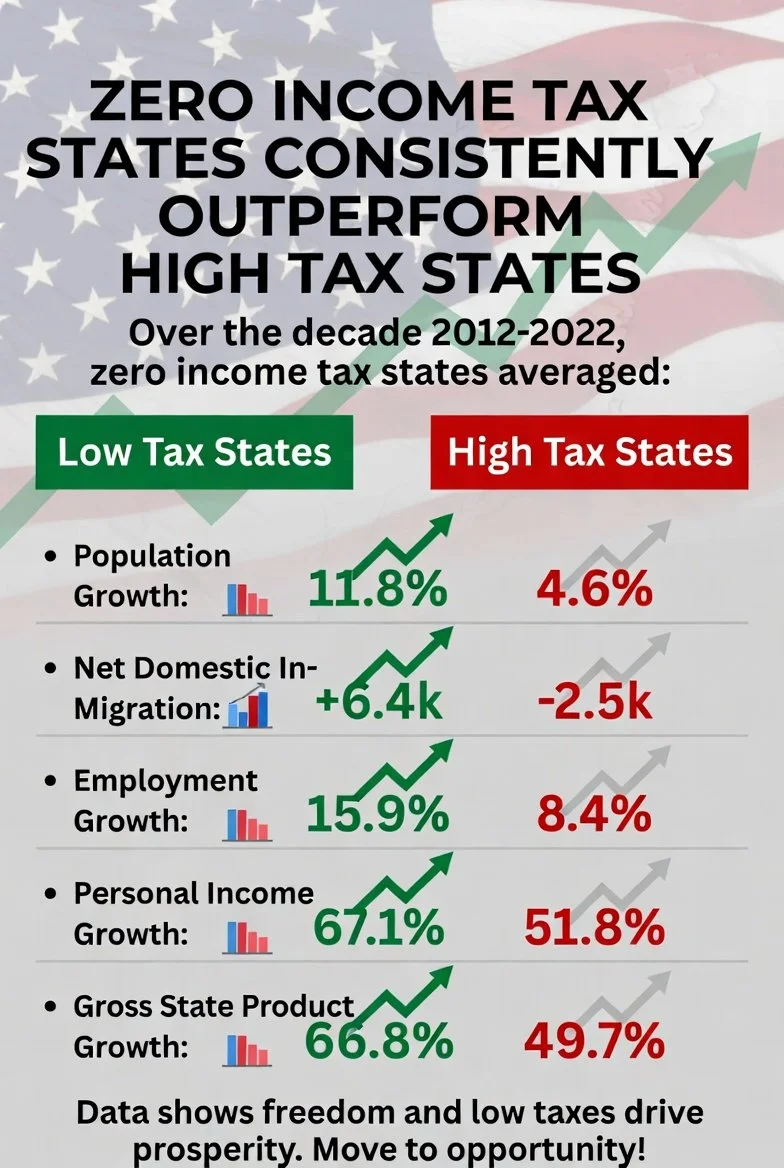

The evidence from other states is decisive. Zero-income-tax states have consistently outperformed high-tax states over the past decade. From 2012 to 2022, they saw stronger population growth (11.8% vs. 4.6%), net domestic in-migration, higher employment growth, and superior personal income and gross state product growth. New York, with one of the highest income tax rates, has lost population and income. Missouri is already bleeding talent and revenue, with IRS data showing net out-migration of adjusted gross income.

Income taxes punish work, saving, and investment. Every dollar taken from Missouri families and businesses reduces economic activity. In contrast, a modernized sales tax base, updated for today’s internet and service economy, closes loopholes that favor out-of-state businesses and billionaires. Critically, new sales tax revenue must flow back to taxpayers through reductions in personal property taxes and real estate taxes. This puts money back in the pockets of hardworking families without net tax increases, while protecting schools.

Missouri cannot afford to cling to an outdated code that drives away jobs, families, and opportunity. HJR 174 modernizes our tax structure, boosts competitiveness with no-income-tax states like Florida and Texas, and puts Missouri families first. It’s time to stop taxing earnings and embrace freedom in buying. Missouri must pass HJR 174 and seize this opportunity for prosperity.

Missouri is Falling Behind: Time to Pass Amendment 5 and Eliminate the Income Tax

Missouri is at a critical crossroads. While nearly a dozen states are actively cutting income tax rates or moving toward full elimination, Missouri remains stuck with a graduated income tax that burdens families, discourages investment, and drives businesses elsewhere.

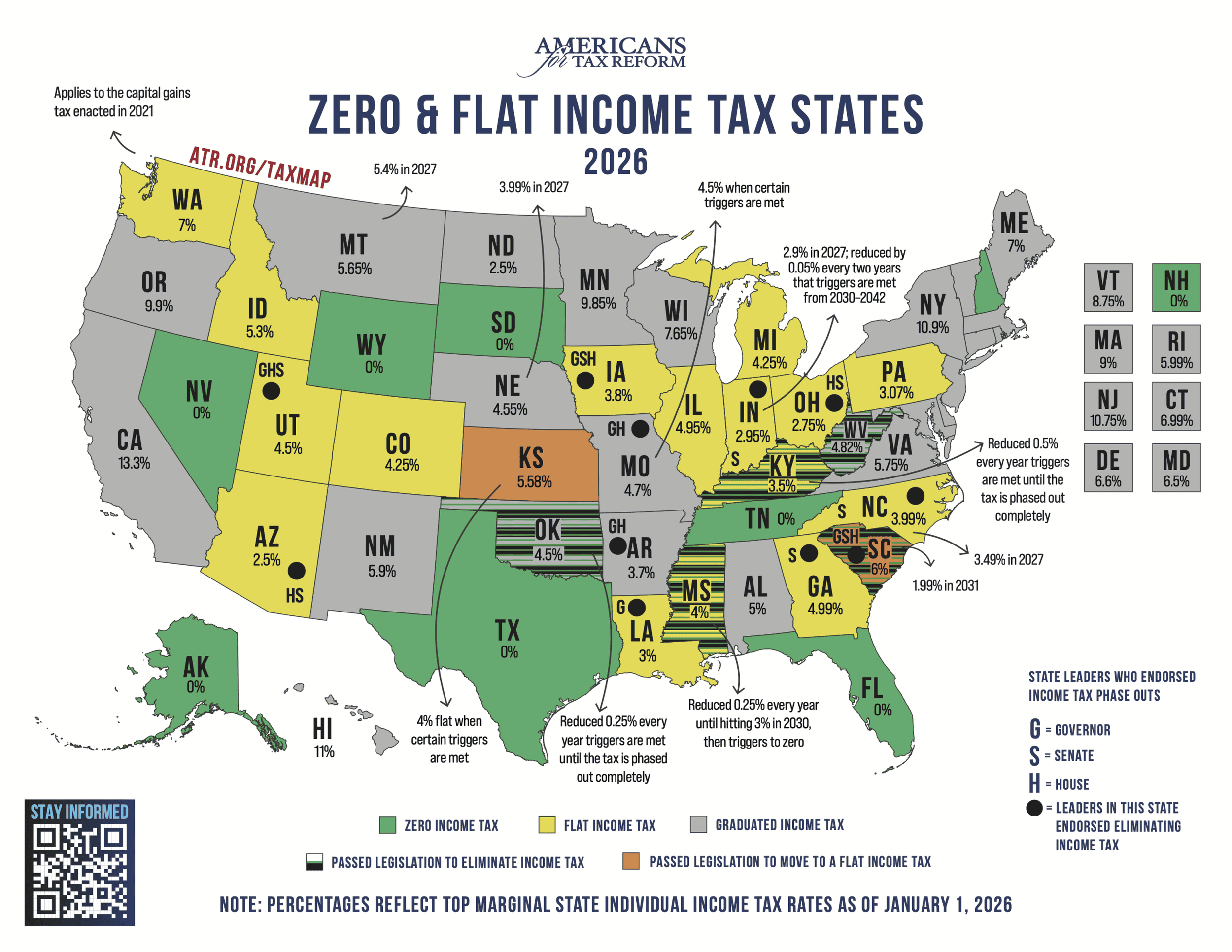

The map below, from Americans for Tax Reform, illustrates the growing national momentum toward tax freedom. Green states have zero income tax. Yellow states have a flat income tax. Gray states still cling to graduated systems like Missouri’s. The map highlights states actively reducing rates or phasing out their income taxes entirely — with many neighboring or competing states making bold moves.

States with no income tax — including Texas, Tennessee, and Florida — continue to lead the nation in population and economic growth. This is no coincidence. Economists have long understood that income taxes are among the most damaging to prosperity because they directly penalize working, saving, investing, and starting or expanding a business. By reducing the rewards for productive activity, high income taxes slow job creation and capital formation.

Look at the map: Texas (0%), Tennessee (0%), Florida (0%), and others are pulling ahead. Several surrounding and competitor states are actively cutting rates or have passed legislation to move toward elimination. Missouri’s current 4.7% top marginal rate, combined with high property taxes and personal property taxes on vehicles and business equipment, makes our state less competitive for relocation and expansion. Families and businesses notice.

That’s why Amendment 5 is so important. This constitutional amendment would advance Missouri’s long-term goal of phasing out the state individual income tax, shifting reliance toward a broader, fairer sales tax base while protecting seniors and low-income Missourians through local offsets and Hancock Amendment safeguards. It positions Missouri to join the ranks of the fastest-growing, most economically dynamic states in the country.

The ATR map makes the case crystal clear. Missouri cannot afford to fall further behind. Other states are choosing tax reform and reaping the benefits of stronger growth, more jobs, and higher take-home pay for families. Missouri families and businesses deserve the same opportunity.

It’s time for Missouri to lead, not lag. Voters should strongly support Amendment 5 this August to secure a brighter, more prosperous future — putting Missouri First, Missouri Forever.

AMENDMENT 5 Does Not Suspend or Eliminate the Hancock Amendment

Missouri voters have long cherished the taxpayer protections enshrined in the Hancock Amendment. Many remember 1980, when voters overwhelmingly approved Article X, Sections 16–24, which imposed historic limits on government growth. Those protections were further strengthened in 1996 by what is often called the “Farmahan Amendment.”

Concerns that any change might open the door to unchecked taxes are understandable and principled. However, claims that AMENDMENT 5 eliminates or suspends the entire Hancock Amendment are simply not true.

The Core Hancock Protections Remain Fully Intact

The original 1980 Hancock Amendment stays completely untouched. Its core provision in Section 18 still caps total state revenues as a fixed share of Missourians’ personal income (based on the FY 1980-81 base ratio of roughly 5.64%). If revenues exceed that limit by 1% or more, the excess must be automatically refunded to taxpayers pro rata through the income tax system.

These bedrock safeguards against runaway government growth, bond exclusions, and the overall revenue ceiling remain exactly as approved by voters decades ago. The legislature cannot simply grow government beyond what personal income growth allows and keep the excess. These protections are not weakened in any way.

What Amendment 5 Actually Does

AMENDMENT 5 creates one narrow, temporary, and purpose-specific exemption — and only from Section 18(e) (the Farmahan Amendment added in 1996).

That provision (which operates “in addition to” the original Section 18) requires voter approval for any bundle of tax or fee increases that would produce new annual revenue above a modest threshold (currently about $154.7 million — the lesser of the inflation-adjusted $50 million figure or 1% of prior total state revenues).

It is a valuable check in normal times. But applying it rigidly here would create an impossible procedural roadblock to meaningful reform.

Why This Targeted Carve-Out Is Necessary and Responsible

Missouri’s tax code is still rooted in the 1930s. It relies far too heavily on taxing work, wages, and investment through the individual income tax. AMENDMENT 5 allows voters to modernize that outdated system by phasing out the state individual income tax while replacing the lost revenue through a broader sales tax base that includes more goods and services.

This is explicitly designed as a revenue-neutral swap. Income tax cuts are fully offset by the new sales tax revenue within the same legislation. Local governments (including schools) are held harmless through required rate adjustments.

Without the Section 18(e) exemption, the sales tax base expansion alone would generate far more than the current $154.7 million threshold in its first full year. The legislature would then be forced to submit the increases to a separate statewide public vote — meaning two elections, years of uncertainty, and almost certainly the death of the reform — even after voters have already approved the overall constitutional framework.

Built-In Safeguards — No Blank Check

The exemption in AMENDMENT 5 is carefully crafted:

It applies only to qualifying legislation passed within five years of the amendment’s effective date.

It covers only bills explicitly tied to reducing or eliminating the income tax.

After that five-year window closes, the full force of Section 18(e) returns for any future tax changes.

The original 1980 Hancock revenue ceiling and automatic refund rules continue without interruption.

This is exactly the kind of practical, limited-government reform the Hancock Amendment was intended to enable — not to freeze Missouri’s tax system in the Great Depression era forever, but to protect citizens from unaccountable spending while allowing smart modernization when the people themselves vote for it at the ballot box.

Honoring the Spirit of Hancock

AMENDMENT 5 honors the spirit of the Hancock Amendment by letting voters decide once on the big-picture tax swap, then giving elected representatives the flexibility to deliver income-tax relief without artificial procedural hurdles that would only apply to this one-time transition.

It keeps the core taxpayer safeguards fully alive while moving Missouri toward a more competitive, family-friendly tax structure that reduces the burden on work and investment.

By supporting AMENDMENT 5, we can modernize Missouri’s tax code responsibly, without tearing down the hard-won protections we value. Focus on the bill text, the fiscal notes, and the actual constitutional language. This is targeted, time-limited reform, not a weakening of our principles.

Vote YES on AMENDMENT 5 to deliver real tax relief while keeping Hancock strong.

Amendment 5: A Historic Opportunity to Slash or Eliminate Personal and Real Property Taxes in Missouri

Amendment 5 creates a powerful constitutional mechanism called “local tax offsets” to ensure that expanding the sales and use tax base, a key step in phasing out Missouri’s individual income tax, does not result in a net tax increase for families and businesses. Instead, it requires local governments to return excess revenue by cutting other taxes, with personal property taxes and residential real property taxes explicitly listed as primary options.

How Local Tax Offsets Work

Under the new Section 26 of Article X in the Missouri Constitution:

The General Assembly may expand sales/use taxes to goods and services not taxed as of January 1, 2015, but only to fund reductions in the state individual income tax and local taxes.

Starting in 2029, every political subdivision (counties, cities, etc.) that collects local sales or use taxes must make annual adjustments. They must reduce revenue from one or more of the following by an amount roughly equal to the new sales tax revenue they receive:

Their own local sales/use tax rate.

Personal property tax levies (cars, boats, business equipment, etc.).

Residential real property tax levies (homes), or operating levies for property taxes, in some interpretations.

Earnings tax rates (where applicable).

Schools are fully protected

No adjustment can reduce funding to public schools. School districts keep any additional sales tax revenue, and their property tax levies remain untouched by these offsets. The state will also adjust certain fixed constitutional sales tax rates (e.g., for parks, conservation, and highways) to prevent windfall collections.

In simple terms, more sales tax revenue flowing to local governments must be offset by giving most of it back through lower taxes elsewhere. Your overall local tax burden stays neutral — or decreases — as the burden shifts from income and property taxes toward consumption taxes.

The Path to Eliminating Property Taxes

Amendment 5 does not automatically abolish property taxes statewide, but it explicitly authorizes and requires local governments to use property tax reductions as a primary tool for offsets. Supporters, including Governor Kehoe and House Republicans, highlight this as a pathway to meaningfully lower, and potentially eliminate, personal property and residential real property taxes.

If new sales tax revenue in a jurisdiction equals or exceeds current collections from the targeted property tax categories, local officials can reduce those levies to zero.

Localities have flexibility: they can mix options (e.g., modest sales tax cuts plus major property tax relief).

Outcomes will vary by locality based on sales tax growth, local decisions, and future implementing legislation.

This “give-back” rule prevents the sales tax expansion from becoming a hidden tax hike. By naming property taxes as a key offset mechanism, Amendment 5 opens the door for Missourians to replace (and in many cases eliminate) burdensome personal and real property taxes while safeguarding school funding and maintaining local revenue.

Bottom line: Amendment 5 delivers real relief for hardworking Missouri families, seniors, and businesses by empowering localities to use new revenue to cut or wipe out property taxes. It advances the “Missouri First – Missouri Forever” vision of lower taxes, economic competitiveness, and putting families first.

Vote YES on Amendment 5 this August to unlock this opportunity for lasting property tax relief.