KNOW BEFORE YOU VOTE

August Ballot Initiatives Voter Guide

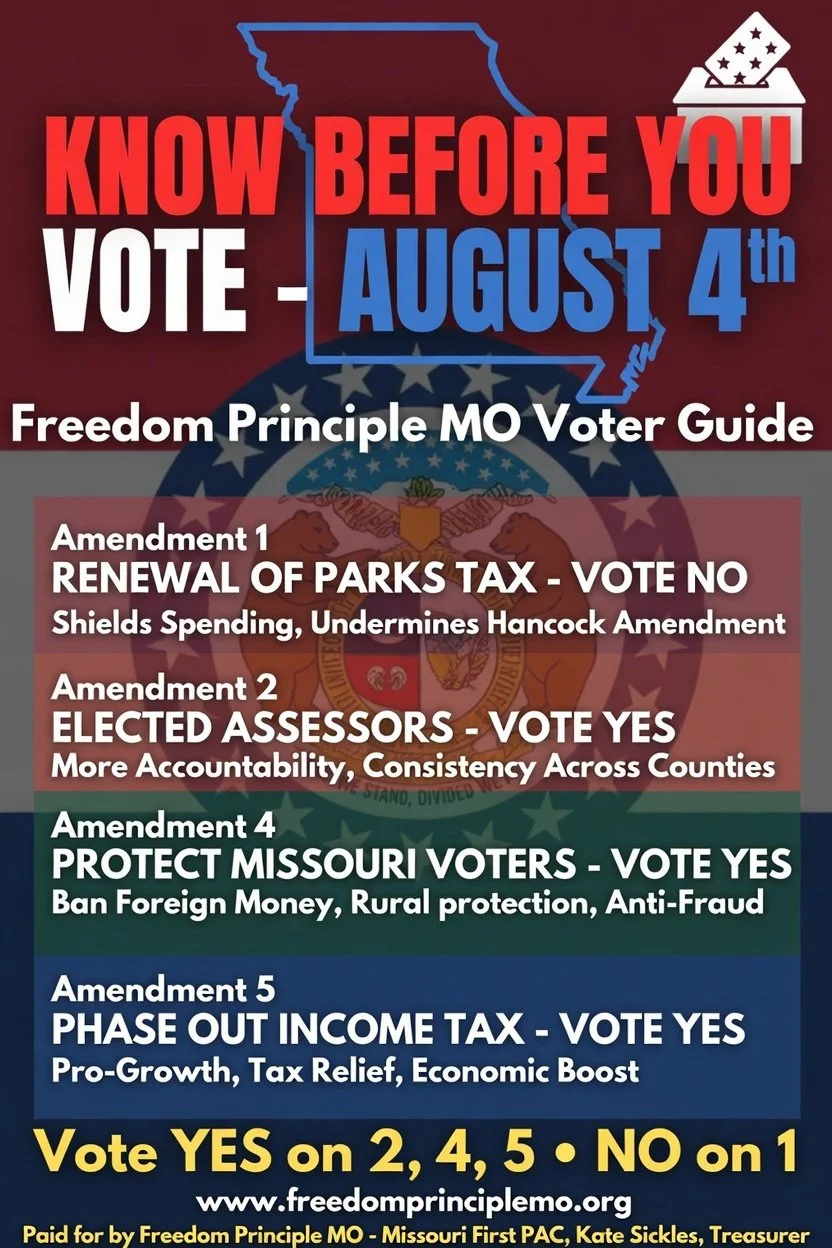

The Freedom Principle MO – Missouri First PAC has reviewed the four constitutional amendments for the August primary ballot. We analyzed the amendments and reviewed external research on each one to provide Missouri voters with the following information and voting recommendations for August 4.

Amendment 1 - Renewal of an existing 0.1% (one-tenth of one percent) sales and use tax dedicated to state parks/historic sites and soil/water conservation programs.

(Oppose)

Reduces pressure on the state to issue refunds to taxpayers: The legislature cannot treat this revenue as general state revenue for the Hancock Amendment calculations.

Restricts legislature from eliminating the Tax: The Legislature cannot eliminate the tax or redirect the funds without a constitutional change.

It shields dedicated spending from overall fiscal oversight: The legislature and governor face less incentive to control overall state spending.

Creates a protected revenue stream outside taxpayer limits: Undermines the spirit of the Hancock Amendment.

Amendment 2 – Requires assessors in Charter Counties to be elected officers (Support)

Increases direct accountability: Elected assessors must answer voters at the ballot box, creating stronger incentives to avoid excessive or unfair increases in property assessments.

Promotes statewide consistency: Aligns charter counties with the standard practice in 113 of Missouri’s 114 counties, where assessors are elected rather than appointed.

Responds to taxpayer frustrations: Directly addresses recent backlash in Jackson County over sharp property value hikes and high appeal volumes by giving residents a direct electoral check.

Enhances democratic principles: Restores voters’ right to choose their assessor, matching the model used across most of the state.

Maintains professional standards: Requires assessors to complete training mandated by general state law, improving qualifications regardless of selection method.

Removes special treatment: Eliminates the unique carve-out that has allowed Jackson County to operate differently from other charter counties.

Amendment 4 – Protect Missouri Voters (Support)

Protects Elections from Foreign Interference: Bans foreign money in ballot measures, addressing national security concerns about adversarial nations (e.g., China, Russia) influencing U.S. state policies. This aligns with federal efforts to limit foreign influence in elections.

Prevents Urban Dominance on Statewide Issues: The "majority in every congressional district" rule ensures rural and diverse parts of Missouri have a real say on constitutional changes, preventing St. Louis/Kansas City metro areas from overriding the rest of the state.

Strengthens Petition Integrity: Criminalizing signature fraud, forgery, and paid signatures deters fraud and builds public trust in the initiative process, which has faced past scandals.

Increases Transparency and Public Input: Mandatory public hearings allow more debate and scrutiny before measures reach the ballot. Providing the full text to voters reduces "surprise" elements and helps informed decision-making.

Legislative Oversight: Gives the General Assembly tools to implement further safeguards without fully blocking citizen initiatives (statutory changes remain easier to pass).

Common-Sense Reforms: Many states have similar protections; this modernizes Missouri's rules without eliminating the initiative process.

Amendment 5 – Phase Out Missouri’s Income Tax and Reduce Property Taxes (Support)

Reduces/Eliminates a Major Tax Burden: Missouri would join states without individual income taxes (e.g., Florida, Texas, Tennessee). This could attract residents, businesses, and high earners, boosting economic growth and population. The mandatory phase-out tied to revenue growth makes it fiscally cautious rather than abrupt.

Revenue Neutrality Safeguards: Income tax cuts are explicitly offset by sales tax base expansions in the same bill, with local offsets. This aims to avoid immediate deficits while shifting the tax base

Local Tax Relief: Forces reductions in property or local sales/earnings taxes when the sales base expands, potentially lowering the overall burden for property owners (with school funding protected).

Limits Future Expansions: The default prohibition on broadening sales taxes to services (unless for this specific purpose) acts as a restraint on government growth.

Pro-Growth and Simplicity: Income taxes discourage work/investment; consumption taxes are often seen as less distortive. Automatic triggers reduce legislative inaction.

School Protection: Explicit carve-out prevents local adjustments from harming education funding.